I was sent a link to this article by a colleague, who was concerned with the boldness of the central claim – that standard economic theory explains nothing about market behaviour. I thought I might as well share the outline of my response here.

I’m far from being a defender of the foundations of mainstream microeconomics. But this attack goes much too quickly, in my view. I find myself in the odd position of defending something I don’t believe in from an attack I think is unfair – indeed counterproductive.

Bichler and Nitzan attack the textbook explanation of prices and quantities as determined by an equilibrium between supply and demand.

Textbook economics represents market equilibrium, for a given commodity, as the intersection between a supply curve and a demand curve. Bichler and Nitzan notice that we never observe demand or supply curves. Of course not, because these represent counterfactuals: the maximum amount consumers would buy if the price were higher/lower, the minimum price firms would charge if the quantity purchased were higher/lower. The famous ‘scissors’ diagram in all the textbooks is not a picture of different states that a system could be in at different times; it’s a picture of a single moment in time, along with a bunch of counterfactuals for that same moment. As Joan Robinson said, time is at right angles to the diagram. So yes, of course supply and demand curves can’t be observed. We don’t observe counterfactuals; we only observe factuals, if I can say that. That is, we only see the price and quantity determined by the actual (factual?) market. So far what Bichler and Nitzan say is obviously true. How do they get from an obvious truth to a devastating critique?

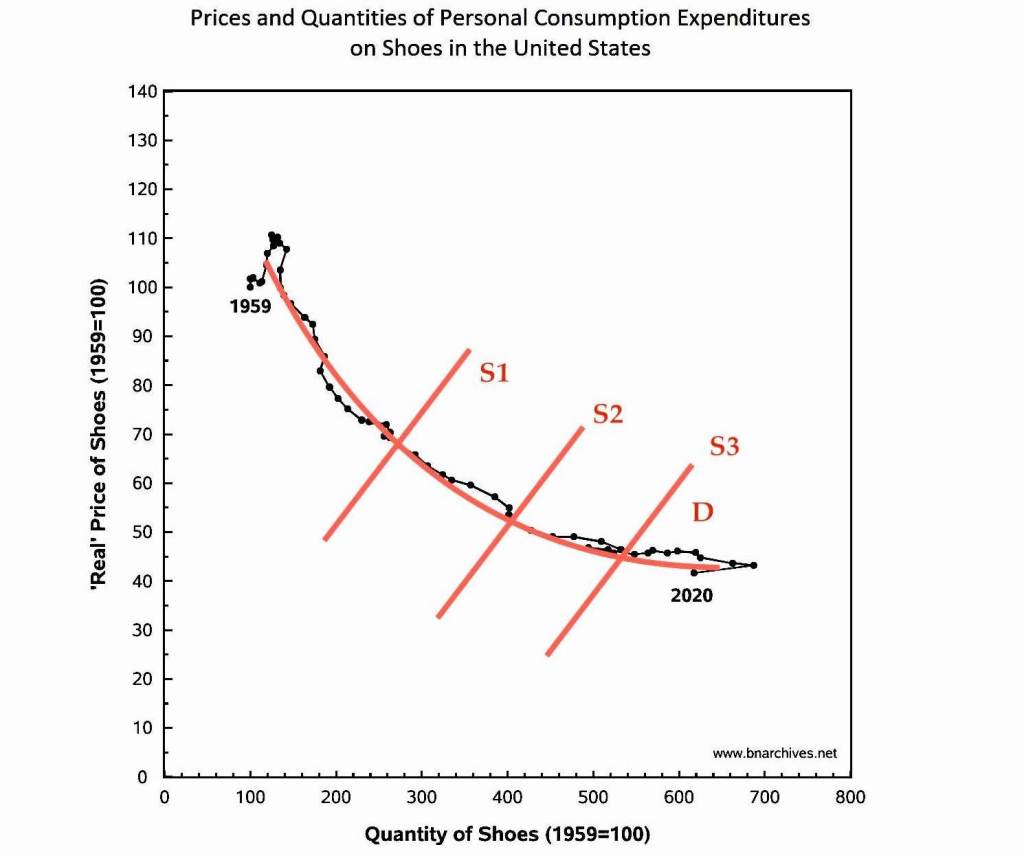

First, they look at a time-series of actual market data. Each point represents the quantity of shoes purchased in a given year (in the US) and the average price paid for a pair of shoes in that year:

They then point out that this data is consistent with each point being a market equilibrium between a different supply and demand curve:

But it’s also consistent with each point being off the equilibrium in any number of ways:

What does this prove? Not much, in my view. It’s hardly news that supply and demand curves can be drawn so as to intersect at any point you like. Since they can’t be observed, they must be constructed on the basis of assumptions. Bichler and Nitzan draw their curves arbitrarily, but they propose that neoclassical economists do the same:

But how did we know what these curves looked like and that they indeed equilibrated at those designated points?

The answer is we didn’t. Just like the neoclassicists, we have no idea what actual demand and supply curves look like. Just like the neoclassicists, we simply plotted them so that they intersected in the observations for 1995, 2000 and 2010. And like the neoclassicists, we did so because these intersections are consistent with the neoclassical doctrine.

But the “just like the neoclassicists” clauses here don’t seem right to me. The ‘neoclassicists’ would surely require some rationale for drawing supply and demand curves a certain way. The curves are counterfactual and unobservable, but they’re meant to represent plausible counterfactuals – plausible given certain assumptions. You can’t just draw them anywhere you like; you need a story about why you draw them where you do.

Now the shifting supply curves drawn by Bichler and Nitzan – S1, S2, S3 – make sense on standard neoclassical assumptions. The years seem roughly to move from left to right in this time-series. A standard assumption is that technology improves over time, and better technology means more efficient, lower-cost production. So this will constantly push the supply curve outwards.

But the shifting demand curves drawn by Bichler and Nitzan – D1, D2, D3 – seem entirely unmotivated. Of course demand changes. Tastes change; changes in income affect demand; changes in one market act unpredictably upon the conditions of all other markets; policy changes have their effects, etc. etc. But I can’t think of any reason the ‘neoclassicists’ would have for supposing a constant outward shift of the demand curve over time. On the contrary, I think the ‘textbook’ assumption would have stable demand – a single demand curve intersected by the outward-shifting supply curves. The curve might jump around a bit, but the jumps could be assumed to go in random directions and thus cancel out over a long period. Then you’d get this:

And this seems to show at least a part of the textbook theory being confirmed in the data. A crucial part of the standard theory is that demand curves slope downwards: as price falls, consumers want to purchase more. Of course here there’s some curve-fitting to make the demand curve match the data. But its basic shape can also be supported on ‘plausible’ assumptions: as markets get saturated, the demand elasticity decreases – thus the flattening out of the curve towards the east.

The above plotting of supply and demand curves isn’t purely arbitrary; it’s based on standard assumptions. So with those (textbook) assumption in place, we have a confirmation of the textbook theory. Nor are the curves simply plotted to match the data, as Bichler and Nitzan’s are; they are justifiable on standard assumptions.

It’s odd to me that Bichler and Nitzan present this data against the mainstream case. I must admit that the part of me that wants textbook microeconomics to fail was disappointed by how well this time-series actually bears out the textbook story. I was actually surprised to see that people really do seem, like the consumers in the textbooks, to buy more shoes as technology reduces the price.

Bichler and Nitzan also cite data showing that the elasticity of demand for different goods varies widely:

This is another case where, aiming to undermine the textbook story, they manage to find data that confirms it! If we were judging the empirical confirmation of a specific economic model we could look at things like the demand elasticity it assumes and see whether this is confirmed in the data. But Bichler and Nitzan are judging textbook microeconomic theory in general. That theory says nothing at all about the specific slope or shape of demand curves. It states only that they slope downwards, and that is, apparently, confirmed in the data.

Standard economic theory makes only very generic predictions – more specific ones need specific models. An example of a generic prediction is what appears to be confirmed in Bichler and Nitzan’s Figure 2: as the price falls, people buy more. Of course the data doesn’t confirm that prediction on its own. You need to assume a stable, downward-sloping demand curve. But Bichler and Nitzan inadvertently find empirical support for that also: they have a table that seems to show that, whatever shape the demand curve might have, it’s generally a downward-sloping one.

To repeat, my reservations about their critique don’t stem from a strong faith in the explanatory power of standard microeconomics. My worry is that the material their critique presents seems to be precisely the sort of thing a textbook might include as a defence of the theory. As a critique of textbook microeconomics, this might be a step backwards.